Structure notes: What they are and who might use them

In the ever growing democratization of finance, structured notes are a product that have remained largely a mystery to the retail investor. These products are still generally required to go through an advisor or bank, and they have yet to receive some of the hype afforded to trends like direct indexing or private investments. But they can still be very powerful tools in the broader financial toolkit.

What are structured notes

Structured notes are effectively a bank issued package of options contracts that create a “defined outcome” across a set of parameters. A mouthful, I know, hopefully I haven’t lost anyone yet. Said more simply: structured notes are typically an investment product that limits the downside risk of an investment while either capping the upside or setting a fixed return on the upside. The two most common note types are Growth and Income, so let’s look at an example for each to help this really click. These are both live offerings as of May 2026.

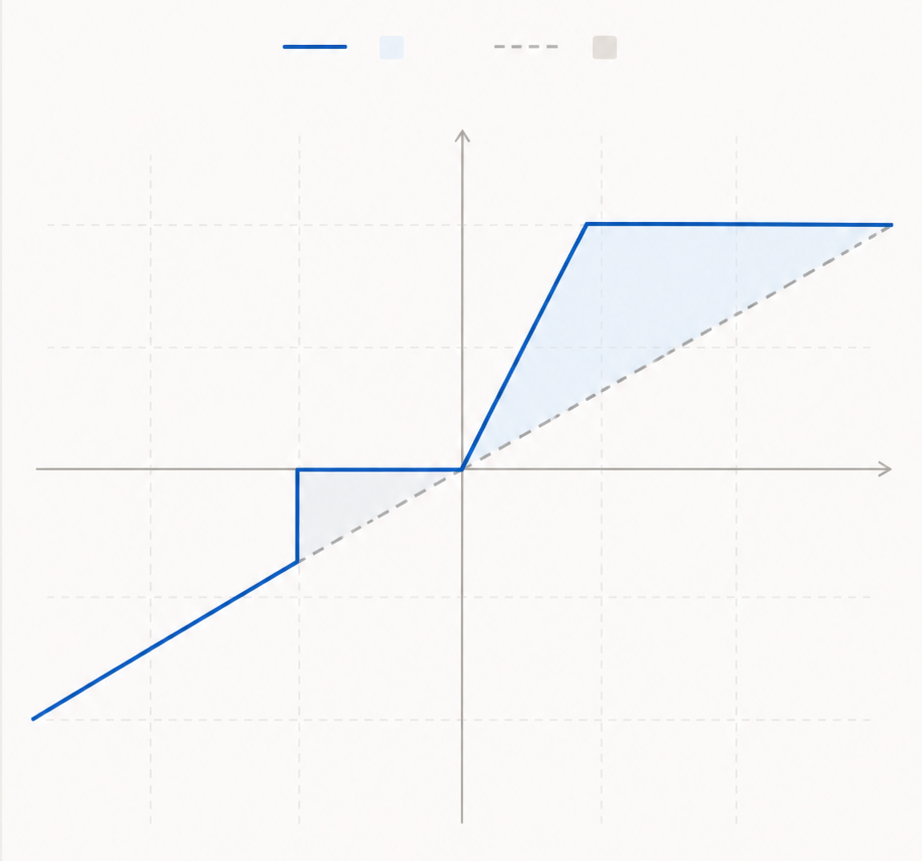

Growth

This is a note that lasts for 3 years, and the underlying indices it tracks are the Nasdaq and S&P 500. The return of the note is based on the worst performer between the Nasdaq and S&P 500. Here are the potential return outcomes after 3 years:

If worst INDEX returns 0 - 18.5%, your return = 2.0x that return (i.e., SPX returns 16%, your return = 32%)

If worst INDEX returns > 18.5%, your return is capped at 37% (even if the worst index returns 100% over that period)

If worst index drops up to 15%, you will get a 0% return (but not a negative return)

If the worst index drops more than 15%, your return is that index performance + 15% (i.e., 20% decline, your return = negative 5%, so you are buffered by 15%)

Growth notes will typically have some form of downside protection, but be linked directly to an index in their returns, capped to a certain level.

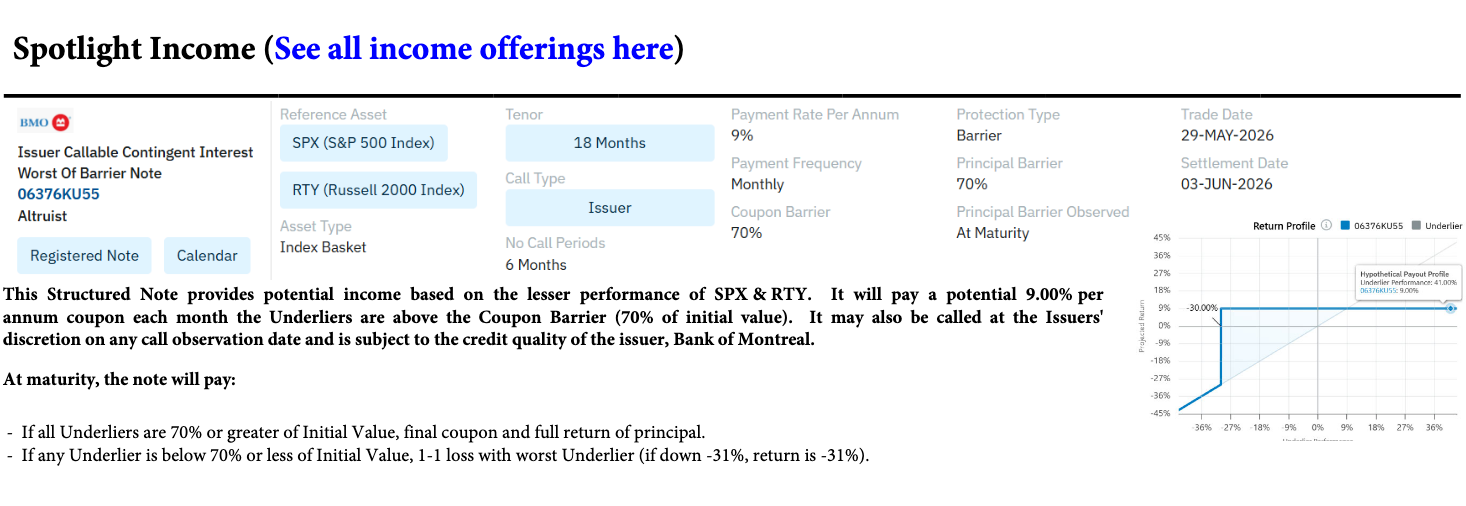

Income

Lucky you, this one comes with a graph! This is a note that lasts for 18 months, and the underlying indices it tracks are the S&P 500 and Russell 2000. The income and principal repayment of the note are based on the worst performer between the S&P 500 and Russell 2000. Here are the potential return outcomes over the life of the note:

If both INDEXES stay above 70% of their initial values on a monthly observation date, you receive the 9% annualized coupon for that month (paid monthly)

The note can be called early by the issuer after the first 6 months; if called, you receive your principal back plus any final coupon payment

If at maturity the worst INDEX is down less than 30% (i.e., remains at or above 70% of initial value), you receive all of your principal back

If at maturity the worst INDEX is down more than 30%, you participate 1:1 in the downside of the worst performer (i.e., if worst index is down 35%, your return = (35%))

Income notes, as you may have deduced, have payout structures that are more akin to bonds or fixed income.

Hidden risks

As discussed, these are generally not investments where you entire principal is protected (although you can actually structure a note to protect your entire principal). But beyond this more obvious point, there are some lesser known risks and considerations to take into account with these products:

Credit risk: Structured notes are backed by the issuing bank. Even if the investment performs as expected, problems at the bank itself could impact repayment.

Limited liquidity: These products are generally designed to be held until maturity. Selling early can be difficult and may result in receiving less than expected or principle loss.

Complexity: Small details in the structure can materially change outcomes. Features like “worst-of,” barriers, and call provisions are important to fully understand before investing. This is why these products generally need to go through an advisor.

Tax treatment: Some structured notes may generate less favorable tax treatment than traditional investments. Tax reporting can also be more complicated depending on the structure.

Early call risk: Some income notes can be called away early by the issuer. This can limit future income potential and force reinvestment at less attractive rates.

Common investor profiles

So who could this be good for? There are a few profiles that we commonly see where this kind of product may be a good fit. As a reminder, this is not personal investment advice, and you should speak with a financial advisor before considering.

Moderately conservative equity investors: Investors who want some stock market exposure but are uncomfortable with full downside participation during market declines. If you’re nervous but don’t want to keep everything in bonds, this is probably the most common profile we see.

Income oriented investors: Investors seeking higher income than traditional bonds or cash equivalents, while accepting some market and issuer risk. This is especially common in tax advantaged accounts that get favorable income note tax treatment (i.e.., IRAs).

Investors that can afford to not sell the note: Individuals who do not anticipate needing liquidity before the note matures and are comfortable locking up capital for a set period. This is also where our previously mentioned “tax advantaged accounts” point may be relevant.

Investors seeking defined outcomes: Investors who prefer knowing the potential upside cap, downside buffer, and income terms upfront rather than taking fully open-ended market exposure.

If you think any of these may describe you, please reach out and we are happy to assess your situation. These products are highly complex, and risks should be fully considered before investing.

This content is for informational purposes only and does not constitute legal or tax advice. Any numbers and estimates are hypothetical. Please consult your advisor before making any financial decisions.